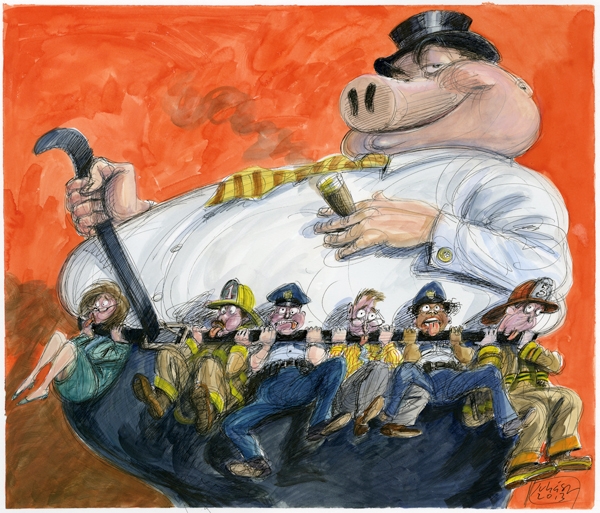

How Wall Street Robs Public Workers

The Article: Looting the Pension Funds by Matt Taibbi in Rolling Stone.

The Text: In the final months of 2011, almost two years before the city of Detroit would shock America by declaring bankruptcy in the face of what it claimed were insurmountable pension costs, the state of Rhode Island took bold action to avert what it called its own looming pension crisis. Led by its newly elected treasurer, Gina Raimondo – an ostentatiously ambitious 42-year-old Rhodes scholar and former venture capitalist – the state declared war on public pensions, ramming through an ingenious new law slashing benefits of state employees with a speed and ferocity seldom before seen by any local government.

Called the Rhode Island Retirement Security Act of 2011, her plan would later be hailed as the most comprehensive pension reform ever implemented. The rap was so convincing at first that the overwhelmed local burghers of her little petri-dish state didn’t even know how to react. “She’s Yale, Harvard, Oxford – she worked on Wall Street,” says Paul Doughty, the current president of the Providence firefighters union. “Nobody wanted to be the first to raise his hand and admit he didn’t know what the fuck she was talking about.”

Soon she was being talked about as a probable candidate for Rhode Island’s 2014 gubernatorial race. By 2013, Raimondo had raised more than $2 million, a staggering sum for a still-undeclared candidate in a thimble-size state. Donors from Wall Street firms like Goldman Sachs, Bain Capital and JPMorgan Chase showered her with money, with more than $247,000 coming from New York contributors alone. A shadowy organization called EngageRI, a public-advocacy group of the 501(c)4 type whose donors were shielded from public scrutiny by the infamous Citizens United decision, spent $740,000 promoting Raimondo’s ideas. Within Rhode Island, there began to be whispers that Raimondo had her sights on the presidency. Even former Obama right hand and Chicago mayor Rahm Emanuel pointed to Rhode Island as an example to be followed in curing pension woes.

What few people knew at the time was that Raimondo’s “tool kit” wasn’t just meant for local consumption. The dynamic young Rhodes scholar was allowing her state to be used as a test case for the rest of the country, at the behest of powerful out-of-state financiers with dreams of pushing pension reform down the throats of taxpayers and public workers from coast to coast. One of her key supporters was billionaire former Enron executive John Arnold – a dickishly ubiquitous young right-wing kingmaker with clear designs on becoming the next generation’s Koch brothers, and who for years had been funding a nationwide campaign to slash benefits for public workers.

Nor did anyone know that part of Raimondo’s strategy for saving money involved handing more than $1 billion – 14 percent of the state fund – to hedge funds, including a trio of well-known New York-based funds: Dan Loeb’s Third Point Capital was given $66 million, Ken Garschina’s Mason Capital got $64 million and $70 million went to Paul Singer’s Elliott Management. The funds now stood collectively to be paid tens of millions in fees every single year by the already overburdened taxpayers of her ostensibly flat-broke state. Felicitously, Loeb, Garschina and Singer serve on the board of the Manhattan Institute, a prominent conservative think tank with a history of supporting benefit-slashing reforms. The institute named Raimondo its 2011 “Urban Innovator” of the year.

The state’s workers, in other words, were being forced to subsidize their own political disenfranchisement, coughing up at least $200 million to members of a group that had supported anti-labor laws. Later, when Edward Siedle, a former SEC lawyer, asked Raimondo in a column for Forbes.com how much the state was paying in fees to these hedge funds, she first claimed she didn’t know. Raimondo later told the Providence Journal she was contractually obliged to defer to hedge funds on the release of “proprietary” information, which immediately prompted a letter in protest from a series of freaked-out interest groups. Under pressure, the state later released some fee information, but the information was originally kept hidden, even from the workers themselves. “When I asked, I was basically hammered,” says Marcia Reback, a former sixth-grade schoolteacher and retired Providence Teachers Union president who serves as the lone union rep on Rhode Island’s nine-member State Investment Commission. “I couldn’t get any information about the actual costs.”

This is the third act in an improbable triple-fucking of ordinary people that Wall Street is seeking to pull off as a shocker epilogue to the crisis era. Five years ago this fall, an epidemic of fraud and thievery in the financial-services industry triggered the collapse of our economy. The resultant loss of tax revenue plunged states everywhere into spiraling fiscal crises, and local governments suffered huge losses in their retirement portfolios – remember, these public pension funds were some of the most frequently targeted suckers upon whom Wall Street dumped its fraud-riddled mortgage-backed securities in the pre-crash years.

Today, the same Wall Street crowd that caused the crash is not merely rolling in money again but aggressively counterattacking on the public-relations front. The battle increasingly centers around public funds like state and municipal pensions. This war isn’t just about money. Crucially, in ways invisible to most Americans, it’s also about blame. In state after state, politicians are following the Rhode Island playbook, using scare tactics and lavishly funded PR campaigns to cast teachers, firefighters and cops – not bankers – as the budget-devouring boogeymen responsible for the mounting fiscal problems of America’s states and cities.

Not only did these middle-class workers already lose huge chunks of retirement money to huckster financiers in the crash, and not only are they now being asked to take the long-term hit for those years of greed and speculative excess, but in many cases they’re also being forced to sit by and watch helplessly as Gordon Gekko wanna-be’s like Loeb or scorched-earth takeover artists like Bain Capital are put in charge of their retirement savings.

It’s a scam of almost unmatchable balls and cruelty, accomplished with the aid of some singularly spineless politicians. And it hasn’t happened overnight. This has been in the works for decades, and the fighting has been dirty all the way.

There’s $2.6 trillion in state pension money under management in America, and there are a lot of fingers in that pie. Any attempt to make a neat Aesop narrative about what’s wrong with the system would inevitably be an oversimplification. But in this hugely contentious, often overheated national controversy – which at times has pitted private-sector workers who’ve mostly lost their benefits already against public-sector workers who are merely about to lose them – two key angles have gone largely unreported. Namely: who got us into this mess, and who’s now being paid to get us out of it.

The siege of America’s public-fund money really began nearly 40 years ago, in 1974, when Congress passed the Employee Retirement Income Security Act, or ERISA. In theory, this sweeping regulatory legislation was designed to protect the retirement money of workers with pension plans. ERISA forces employers to provide information about where pension money is being invested, gives employees the right to sue for breaches of fiduciary duty, and imposes a conservative “prudent man” rule on the managers of retiree funds, dictating that they must make sensible investments and seek to minimize loss. But this landmark worker-protection law left open a major loophole: It didn’t cover public pensions. Some states were balking at federal oversight, and lawmakers, naively perhaps, simply never contemplated the possibility of local governments robbing their own workers.

Politicians quickly learned to take liberties. One common tactic involved illegally borrowing cash from public retirement funds to finance other budget needs. For many state pension funds, a significant percentage of the kitty is built up by the workers themselves, who pitch in as little as one and as much as 10 percent of their income every year. The rest of the fund is made up by contributions from the taxpayer. In many states, the amount that the state has to kick in every year, the Annual Required Contribution (ARC), is mandated by state law.

Chris Tobe, a former trustee of the Kentucky Retirement Systems who blew the whistle to the SEC on public-fund improprieties in his state and wrote a book called Kentucky Fried Pensions, did a careful study of states and their ARCs. While some states pay 100 percent (or even more) of their required bills, Tobe concluded that in just the past decade, at least 14 states have regularly failed to make their Annual Required Contributions. In 2011, an industry website called 24/7 Wall St. compiled a list of the 10 brokest, most busted public pensions in America. “Eight of those 10 were on my list,” says Tobe.

Among the worst of these offenders are Massachusetts (made just 27 percent of its payments), New Jersey (33 percent, with the teachers’ pension getting just 10 percent of required payments) and Illinois (68 percent). In Kentucky, the state pension fund, the Kentucky Employee Retirement System (KERS), has paid less than 50 percent of its ARCs over the past 10 years, and is now basically butt-broke – the fund is 27 percent funded, which makes bankrupt Detroit, whose city pension is 77 percent full, look like the sultanate of Brunei by comparison.

Here’s what this game comes down to. Politicians run for office, promising to deliver law and order, safe and clean streets, and good schools. Then they get elected, and instead of paying for the cops, garbagemen, teachers and firefighters they only just 10 minutes ago promised voters, they intercept taxpayer money allocated for those workers and blow it on other stuff. It’s the governmental equivalent of stealing from your kids’ college fund to buy lap dances. In Rhode Island, some cities have underfunded pensions for decades. In certain years zero required dollars were contributed to the municipal pension fund. “We’d be fine if they had made all of their contributions,” says Stephen T. Day, retired president of the Providence firefighters union. “Instead, after they took all that money, they’re saying we’re broke. Are you fucking kidding me?”

There’s an arcane but highly disturbing twist to the practice of not paying required contributions into pension funds: The states that engage in this activity may also be committing securities fraud. Why? Because if a city or state hasn’t been making its required contributions, and this hasn’t been made plain to the ratings agencies, then that same city or state is actually concealing what in effect are massive secret loans and is actually far more broke than it is representing to investors when it goes out into the world and borrows money by issuing bonds.

Some states have been caught in the act of doing this, but the penalties have been so meager that the practice can be considered quasi-sanctioned. For example, in August 2010, the SEC reprimanded the state of New Jersey for serially lying about its failure to make pension contributions throughout the 2000s. “New Jersey failed to provide certain present and historical financial information regarding its pension funding in bond-disclosure documents,” the SEC wrote, in seemingly grave language. “The state was aware of?.?.?.?the potential effects of the underfunding.” Illinois was similarly reprimanded by the SEC for lying about its failure to make its required pension contributions. But in neither of these cases were the consequences really severe. So far, states get off with no monetary fines at all. “The SEC was mistaken if they think they sent a message to other states,” Tobe says.

But for all of this, state pension funds were more or less in decent shape prior to the financial crisis of 2008. The country, after all, had been in a historic bull market for most of the 1990s and 2000s and politicians who underpaid the ARCs during that time often did so assuming that the good times would never end. In fact, prior to the crash, state pension funds nationwide were cumulatively running a surplus. But then the crash came, and suddenly states everywhere were in a real, no-joke fiscal crisis. Tax revenues went in the crapper, and someone had to take the hit. But who? Cuts to corporate welfare and a rolled-up-newspaper whack of new taxes on the guilty finance sector seemed a good place to start, but it didn’t work out that way. Instead, it was then that the legend of pension unsustainability was born, with the help of a pair of unlikely allies.

Most people think of Pew Charitable Trusts as a centrist, nonpartisan organization committed to sanguine policy analysis and agnostic number crunching. It’s an odd reputation for an organization that was the legacy of J. Howard Pew, president of Sun Oil (the future Sunoco) during its early 20th-century petro-powerhouse days and a kind of australopithecine precursor to a Tea Party leader. Pew had all the symptoms: an obsession with the New Deal as a threat to free society, a keen appreciation for unreadable Austrian economist F.A. Hayek and a hoggish overuse of the word “freedom.” Pew and his family left nearly $1 billion to a series of trusts, one of which was naturally called the “Freedom Trust,” whose mission was, in part, to combat “the false promises of socialism and a planned economy.”

Still, for decades Pew trusts engaged in all sorts of worthy endeavors, including everything from polling to press criticism. In 2007, Pew began publishing an annual study called “The Widening Gap,” which aimed to use states’ own data to show the “gap” between present pension-fund levels and future obligations. The study quickly became a leading analysis of the “unfunded liability” question.

In 2011, Pew began to align itself with a figure who was decidedly neither centrist nor nonpartisan: 39-year-old John Arnold, whom CNN/Money described (erroneously) as the “second-youngest self-made billionaire in America,” after Mark Zuckerberg. Though similar in wealth and youth, Arnold presented the stylistic opposite of Zuckerberg’s signature nerd chic: He’s a lipless, eager little jerk with the jug-eared face of a Division III women’s basketball coach, exactly what you’d expect a former Enron commodities trader to look like. Anyone who has seen the Oscar-winning documentary The Smartest Guys in the Room and remembers those tapes of Enron traders cackling about rigging energy prices on “Grandma Millie” and jamming electricity rates “right up her ass for fucking $250 a megawatt hour” will have a sense of exactly what Arnold’s work environment was like.

In fact, in the book that the movie was based on, the authors portray Arnold bragging about his minions manipulating energy prices, praising them for “learning how to use the Enron bat to push around the market.” Those comments later earned Arnold visits from federal investigators, who let him get away with claiming he didn’t mean what he said.

As Enron was imploding, Arnold played a footnote role, helping himself to an $8 million bonus while the company’s pension fund was vaporizing. He and other executives were later rebuked by a bankruptcy judge for looting their own company along with other executives. Public pension funds nationwide, reportedly, lost more than $1.5 billion thanks to their investments in Enron.

In 2002, Arnold started a hedge fund and over the course of the next few years made roughly a $3 billion fortune as the world’s most successful natural-gas trader. But after suffering losses in 2010, Arnold bowed out of hedge-funding to pursue “other interests.” He had created the Arnold Foundation, an organization dedicated, among other things, to reforming the pension system, hiring a Republican lobbyist and former chief of staff to Dick Armey named Denis Calabrese, as well as Dan Liljenquist, a Utah state senator and future Tea Party challenger to Orrin Hatch.

Soon enough, the Arnold Foundation released a curious study on pensions. On the one hand, it admitted that many states had been undercontributing to their pension funds for years. But instead of proposing that states correct the practice, the report concluded that “the way to create a sound, sustainable and fair retirement-savings program is to stop promising a [defined] benefit.”

In 2011, Arnold and Pew found each other. As detailed in a new study by progressive think tank Institute for America’s Future, Arnold and Pew struck up a relationship – and both have since been proselytizing pension reform all over America, including California, Florida, Kansas, Arizona, Kentucky and Montana. Few knew that Pew had a relationship with a right-wing, anti-pension zealot like Arnold. “The centrist reputation of Pew was a key in selling a lot of these ideas,” says Jordan Marks of the National Public Pension Coalition. Later, a Pew report claimed that the national “gap” between pension assets and future liabilities added up to some $757 billion and dryly insisted the shortfall was unbridgeable, minus some combination of “higher contributions from taxpayers and employees, deep benefit cuts and, in some cases, changes in how retirement plans are structured and benefits are distributed.”

What the study didn’t say was that this supposedly massive gap could all be chalked up to the financial crisis, which, of course, had been caused almost entirely by the greed and wide-scale fraud of the financial-services industry – particularly with regard to state pension funds.

A study by noted economist Dean Baker at the Center for Economic Policy and Research bore this out. In February 2011, Baker reported that, had public pension funds not been invested in the stock market and exposed to mortgage-backed securities, there would be no shortfall at all. He said state pension managers were of course somewhat to blame, but only “insofar as they exercised poor judgment in buying the [finance] industry’s services.”

In fact, Baker said, had public funds during the crash years simply earned modest returns equal to 30-year Treasury bonds, then public-pension assets would be $850 billion richer than they were two years after the crash. Baker reported that states were short an additional $80 billion over the same period thanks to the fact that post-crash, cash-strapped states had been paying out that much less of their mandatory ARC payments.

So even if Pew’s numbers were right, the “unfunded liability” crisis had nothing to do with the systemic unsustainability of public pensions. Thanks to a deadly combination of unscrupulous states illegally borrowing from their pensioners, and unscrupulous banks whose mass sales of fraudulent toxic subprime products crashed the market, these funds were out some $930 billion. Yet the public was being told that the problem was state workers’ benefits were simply too expensive.

In a way, this was a repeat of a shell game with retirement finance that had been going on at the federal level since the Reagan years. The supposed impending collapse of Social Security, which actually should be running a surplus of trillions of dollars, is now repeated as a simple truth. But Social Security wouldn’t be “collapsing” at all had not three decades of presidents continually burgled the cash in the Social Security trust fund to pay for tax cuts, wars and God knows what else. Same with the alleged insolvencies of state pension programs. The money may not be there, but that’s not because the program is unsustainable: It’s because bankers and politicians stole the money.

Still, the public mostly bought the line being sold by Arnold, Pew and other anti-pension figures like the Koch brothers. To most, it didn’t matter who was to blame: What mattered is that the money was gone, and there seemed to be only two possible paths forward. One led to bankruptcy, a real-enough threat that had already ravaged places like Vallejo, California; Jefferson County, Alabama; and, this summer, Detroit. In Rhode Island, the tiny town of Central Falls went bust in 2011, and even after a court-ordered plan lifted the town out of bankruptcy in 2012, the “rescue” left pensions slashed as much as 55 percent. “You had guys who were living off $24,000, and now they’re getting $12,000,” says Day. Though Day and his fellow retirees are still fighting reform, he says other union workers might rather settle than file bankruptcy. Holding up an infamous local-newspaper picture of a retired Central Falls policeman in a praying posture, as though begging not to have his whole pension taken away, Day sighs. “Guys take one look at this picture and that’s it. They’re terrified.”

Such images chilled many public workers into accepting the second path – the kind of pension reform meagerly touted by one-percent-friendly politicians like Gina Raimondo. Anyone could see that “reform” meant giving up cash. But the other parts of these schemes were murkier. Most pension-reform proposals required that states must go after higher returns by seeking out “alternative investments,” which sounds harmless enough. But we are now finding out what that term actually means – and it’s a little north of harmless.

One of the most garish early experiments in “alternative investments” came in Ohio in the late 1990s, after the Republican-controlled state assembly passed a law loosening restrictions on what kinds of things state funds could invest in. Sometime later, an investigation by the Toledo Blade revealed that the Ohio Bureau of Workers’ Compensation had bought into rare-coin funds run by a GOP fundraiser named Thomas Noe. Through Noe, Ohio put $50 million into coins and “other collectibles” – including Beanie Babies.

The scandal had repercussions all over the country, but not what you’d expect. James Drew, one of the reporters who broke the story, notes that a consequence of “Coingate” was that states stopped giving out information about where public money is invested. “If they learned anything, it’s not to stop doing it, but to keep it secret,” says Drew.

In fact, in recent years more than a dozen states have carved out exemptions for hedge funds to traditional Freedom of Information Act requests, making it impossible in some cases, if not illegal, for workers to find out where their own money has been invested.

The way this works, typically, is simple: A hedge fund will refuse to take a state’s business unless it first provides legal guarantees that information about its investments won’t be disclosed to the public. The ostensible justifications for these outrageous laws are usually that disclosing commercial information about hedge funds would place them at a “competitive disadvantage.”

In 2010, the University of California reinvested its pension fund with a venture-capital group called Sequoia Capital, which in turn is a backer of a firm called Think Finance, whose business is payday lending – a form of short-term, extremely high-interest rate lending that’s basically loan-sharking without the leg-breaking, and is banned in 15 states and D.C. According to American Banker, Think Finance partnered with a Native American tribe to get around state interest-rate caps; someone borrowing $250 in its “plain green loans” program would owe $440 after 16 weeks, for a tidy annual percentage rate of 379 percent. In a more recent case, the pension fund of L.A. County union workers invested in an Embassy Suites hotel that is trying to prevent janitors and other employees from organizing. California passed a law in 2005 making hedge-fund investments secret.

The American Federation of Teachers this spring released a list of financiers who had been connected with lobbying efforts against defined-benefit plans. Included on that list was hedge-funder Loeb of Third Point Capital, who sits on the board of StudentsFirstNY, a group that advocates for an end to these traditional plans for public workers – that is, pensions that promise a guaranteed payout based on one’s salary and years of service. When Rhode Island union rep Reback complained about hiring funds whose managers had anti-labor histories, she was told the state couldn’t make decisions based on political leanings of fund managers. That same month, Rhode Island moved to disinvest its workers’ money from firearms distributors in the wake of the Sandy Hook shooting.

Hedge funds have good reason to want to keep their fees hidden: They’re insanely expensive. The typical fee structure for private hedge-fund management is a formula called “two and twenty,” meaning the hedge fund collects a two percent fee just for showing up, then gets 20 percent of any profits it earns with your money. Some hedge funds also charge a mysterious third fee, called “fund expenses,” that can run as high as half a percent – Loeb’s Third Point, for instance, charged Rhode Island just more than half a percent for “fund expenses” last year, or about $350,000. Hedge funds will also pass on their trading costs to their clients, a huge additional line item that can come to an extra percent or more and is seldom disclosed. There are even fees states pay for withdrawing from certain hedge funds.

In public finance, hedge funds will sometimes give slight discounts, but the numbers are still enormous. In Rhode Island, over the course of 20 years, Siedle projects that the state will pay $2.1 billion in fees to hedge funds, private-equity funds and venture-capital funds. Why is that number interesting? Because it very nearly matches the savings the state will be taking from workers by freezing their Cost of Living Adjustments – $2.3 billion over 20 years.

“That’s some ‘reform,'” says Siedle.

“They pretty much took the COLA and gave it to a bunch of billionaires,” hisses Day, Providence’s retired firefighter union chief.

When asked to respond to criticisms that the savings from COLA freezes could be seen as going directly into the pockets of billionaires, treasurer Raimondo replied that it was “very dangerous to look at fees in a vacuum” and that it’s worth paying more for a safer and more diverse portfolio. She compared hedge funds – inherently high-risk investments whose prospectuses typically contain front-page disclaimers saying things like, WARNING: YOU MAY LOSE EVERYTHING – to snow tires. “Sure, you pay a little more,” she says. “But you’re really happy you have them when the roads are slick.”

Raimondo recently criticized the high-fee structure of hedge funds in the Wall Street Journal and told Rolling Stone that “‘two and twenty’?doesn’t make sense anymore,” although she hired several funds at precisely those fee levels back before she faced public criticism on the issue. She did add that she was monitoring the funds’ performance. “If they underperform, they’re out,” she says.

And underperforming is likely. Even though hedge funds can and sometimes do post incredible numbers in the short-term – Loeb’s Third Point notched a 41 percent gain for Rhode Island in 2010; the following year, it earned -0.54 percent. On Wall Street, people are beginning to clue in to the fact – spikes notwithstanding – that over time, hedge funds basically suck. In 2008, Warren Buffett famously placed a million-dollar bet with the heads of a New York hedge fund called Protégé Partners that the S&P 500 index fund – a neutral bet on the entire stock market, in other words – would outperform a portfolio of five hedge funds hand-picked by the geniuses at Protégé.

Five years later, Buffett’s zero-effort, pin-the-tail-on-the-stock-market portfolio is up 8.69 percent total. Protégé’s numbers are comical in comparison; all those superminds came up with a 0.13 percent increase over five long years, meaning Buffett is beating the hedgies by nearly nine points without lifting a finger.

Union leaders all over the country have started to figure out the perils of hiring a bunch of overpriced Wall Street wizards to manage the public’s money. Among other things, investing with hedge funds is infinitely more expensive than investing with simple index funds. On Wall Street and in the investment world, the management price is measured in something called basis points, a basis point equaling one hundredth of one percent. So a state like Rhode Island, which is paying a two percent fee to hedge funds, is said to be paying an upfront fee of 200 basis points.

How much does it cost to invest public money in a simple index fund? “We’ve paid as little as .875 of a basis point,” says William Atwood, executive director of the Illinois State Board of Investment. “At most, five basis points.”

So at the low end, Atwood is paying 200 times less than the standard two percent hedge-fund fee. As an example, Atwood says, the state of Illinois paid a fee of just $57,000 last year on $550 million of public money they put into an S&P 500 index fund, which, again, is exactly the sort of plain-vanilla investment that Warren Buffett used to publicly kick the ass of Wall Street’s cockiest hedge fund.

The fees aren’t even the only costs of “alternative investments.” Many states have engaged middlemen called “placement agents” to hire hedge funds, and those placement agents – typically people with ties to state investment boards – are themselves paid enormous sums, often in the millions, just to “introduce” hedge funds to politicians holding the checkbook.

In Kentucky, Tobe and Siedle found that KRS, the state pension funds, had paid a whopping $14 million to placement agents between 2004 and 2009. In Atlanta, a member of the city pension board complained to the SEC that the city had hired a consultant, Larry Gray, who convinced the city pension fund to invest $28 million in a hedge fund he himself owned. Raimondo says she never hired placement agents, but the state did pay a $450,000 consulting fee to a firm called Cliffwater LLC.

Doughty says the endless system of highly paid middlemen reminds him of old slapstick comedies. “It’s like the Three Stooges,” he says. “When you ask them what happened, they’re all pointing in different directions, like, ‘He did it!'”

Even worse, placement agents are also often paid by the alternative investors. In California, the Apollo private-equity firm paid a former CalPERS board member named Alfred Villalobos a staggering $48 million for help in securing investments from state pensions, and Villalobos delivered, helping Apollo receive $3 billion of CalPERS money. Villalobos got indicted in that affair, but only because he’d lied to Apollo about disclosing his fees to CalPERS. Otherwise, despite the fact that this is in every way basically a crude kickback scheme, there’s no law at all against a placement agent taking money from a finance firm. The Government Accountability Office has condemned the practice, but it goes on.

“It’s a huge conflict of interest,” says Siedle.

So when you invest your pension money in hedge funds, you might be paying a hundred times the cost or more, you might be underperforming the market, you may be supporting political movements against you, and you often have to pay what effectively is a bribe just for the privilege of hiring your crappy overpaid money manager in the first place. What’s not to like about that? Who could complain?

Once upon a time, local corruption was easy. “It was votes for jobs,” Doughty says with a sigh. A ward would turn out for a councilman, the councilman would come back with jobs from city-budget contracts – that was the deal. What’s going on with public pensions is a more confusing modern version of that local graft. With public budgets carefully scrutinized by everyone from the press to regulators, the black box of pension funds makes it the only public treasure left that’s easy to steal. Politicians quietly borrow millions from these funds by not paying their ARCs, and it’s that money, plus the savings from cuts made to worker benefits in the name of “emergency” pension reform, that pays for an apparently endless regime of corporate tax breaks and handouts.

A notorious example in Rhode Island is, of course, 38 Studios, the doomed video-game venture of blabbering, Christ-humping ex-Red Sox pitcher Curt Schilling, who received a $75 million loan guarantee from the state at a time when local politicians were pleading poverty. “This whole thing isn’t just about cutting payments to retirees,” says syndicated columnist David Sirota, who authored the Institute for America’s Future study on Arnold and Pew. “It’s about preserving money for corporate welfare.” Their study estimates states spend up to $120 billion a year on offshore tax loopholes and gifts to dingbats like Schilling and other subsidies – more than two and a half times as much as the $46 billion a year Pew says states are short on pension payments.

The bottom line is that the “unfunded liability” crisis is, if not exactly fictional, certainly exaggerated to an outrageous degree. Yes, we live in a new economy and, yes, it may be time to have a discussion about whether certain kinds of public employees should be receiving sizable benefit checks until death. But the idea that these benefit packages are causing the fiscal crises in our states is almost entirely a fabrication crafted by the very people who actually caused the problem. It’s like Voltaire’s maxim about noses having evolved to fit spectacles, so therefore we wear spectacles. In this case, we have an unfunded-pension-liability problem because we’ve been ripping retirees off for decades – but the solution being offered is to rip them off even more.

Everybody following this story should remember what went on in the immediate aftermath of the crash of 2008, when the federal government was so worried about the sanctity of private contracts that it doled out $182 billion in public money to AIG. That bailout guaranteed that firms like Goldman Sachs and Deutsche Bank could be paid off on their bets against a subprime market they themselves helped overheat, and that AIG executives could be paid the huge bonuses they naturally deserved for having run one of the world’s largest corporations into the ground. When asked why the state was paying those bonuses, Obama economic adviser Larry Summers said, “We are a country of law.?.?.?.?The government cannot just abrogate contracts.”

Now, though, states all over the country are claiming they not only need to abrogate legally binding contracts with state workers but also should seize retirement money from widows to finance years of illegal loans, giant fees to billionaires like Dan Loeb and billions in tax breaks to the Curt Schillings of the world. It ain’t right. If someone has to tighten a belt or two, let’s start there. If we’ve still got a problem after squaring those assholes away, that’s something that can be discussed. But asking cops, firefighters and teachers to take the first hit for a crisis caused by reckless pols and thieves on Wall Street is low, even by American standards.